Solving QUBO problems using QAOA#

Overview#

Here we show how to solve a quadratic unconstrained binary optimization (QUBO) problem using QAOA. Later on below we will extend this to show how to solve binary Markowitz portfolio optimization problems.

Consider minimizing the following 2x2 QUBO objective function:

\(\begin{pmatrix}x_1 & x_2\end{pmatrix}\begin{pmatrix}-5& -2 \\-2 & 6\end{pmatrix}\begin{pmatrix}x_1\\x_2\end{pmatrix} = -5x_1^2 -4x_1x_2 +6x_2^2\)

Clearly this is minimized at \((x_1,x_2) = (1,0)\), with corresponding objective function value of \(-5\)

We first convert this to an Ising Hamiltonian by mapping \(x_i\rightarrow \frac{I-Z_i}{2}\)

This gives

which simplifies to

The \(-I/2\) term is simply a constant offset, so we can solve the problem by finding the minimum of

Note that the minimum should correspond to the computational basis state \(|10\rangle\), and the corresponding true objective function value should be \(-4.5\) (ignoring the offset value of \(-1/2\))

Setup#

[ ]:

import tensorcircuit as tc

import numpy as np

import tensorflow as tf

import matplotlib.pyplot as plt

from functools import partial

[2]:

# we first manually encode the terms (-7/2) Z_1 - 2 Z_2 - Z_1Z_2 as:

pauli_terms = [

[1, 0],

[0, 1],

[1, 1],

] # see the TensorCircuit whitepaper for 'pauli structures'

weights = [7 / 2, -2, -1]

# see below for a function to generate the pauli terms and weights from the QUBO matrix

[3]:

# Now we define the QAOA ansatz of depth nlayers

def QAOA_from_Ising(params, nlayers, pauli_terms, weights):

nqubits = len(pauli_terms[0])

c = tc.Circuit(nqubits)

for i in range(nqubits):

c.h(i)

for j in range(nlayers):

for k in range(len(pauli_terms)):

term = pauli_terms[k]

index_of_ones = []

for l in range(len(term)):

if term[l] == 1:

index_of_ones.append(l)

if len(index_of_ones) == 1:

c.rz(index_of_ones[0], theta=2 * weights[k] * params[2 * j])

elif len(index_of_ones) == 2:

c.exp1(

index_of_ones[0],

index_of_ones[1],

unitary=tc.gates._zz_matrix,

theta=weights[k] * params[2 * j],

)

else:

raise ValueError("Invalid number of Z terms")

for i in range(nqubits):

c.rx(i, theta=params[2 * j + 1]) # mixing terms

return c

For a general state that is the output of a quantum circuit c, we first define the corresponding loss with respect to the Ising Hamiltonian.

[4]:

def Ising_loss(c, pauli_terms, weights):

loss = 0.0

for k in range(len(pauli_terms)):

term = pauli_terms[k]

index_of_ones = []

for l in range(len(term)):

if term[l] == 1:

index_of_ones.append(l)

if len(index_of_ones) == 1:

delta_loss = weights[k] * c.expectation_ps(z=[index_of_ones[0]])

else:

delta_loss = weights[k] * c.expectation_ps(

z=[index_of_ones[0], index_of_ones[1]]

)

loss += delta_loss

return K.real(loss)

For the particular case of a circuit corresponding to a QAOA ansatz this is:

[5]:

def QAOA_loss(nlayers, pauli_terms, weights, params):

c = QAOA_from_Ising(params, nlayers, pauli_terms, weights)

return Ising_loss(c, pauli_terms, weights)

[6]:

K = tc.set_backend("tensorflow")

[7]:

def QAOA_solve(pauli_terms, weights, nlayers, iterations):

print_every = 100

learning_rate = 1e-2

loss_val_grad = K.value_and_grad(partial(QAOA_loss, nlayers, pauli_terms, weights))

loss_val_grad_jit = K.jit(loss_val_grad)

opt = K.optimizer(tf.keras.optimizers.Adam(learning_rate))

params = K.implicit_randn(shape=[2 * nlayers], stddev=0.5)

print(f"initial params: {params}")

for i in range(iterations):

loss, grads = loss_val_grad_jit(params)

if i % print_every == 0:

print(K.numpy(loss))

params = opt.update(grads, params)

return params

[12]:

iterations = 500

nlayers = 2

final_params = QAOA_solve(pauli_terms, weights, nlayers, iterations)

initial params: [ 0.39931756 -0.49578992 -0.22545011 -0.40585193]

-2.1728685

-4.177884

-4.2291102

-4.2291365

-4.229136

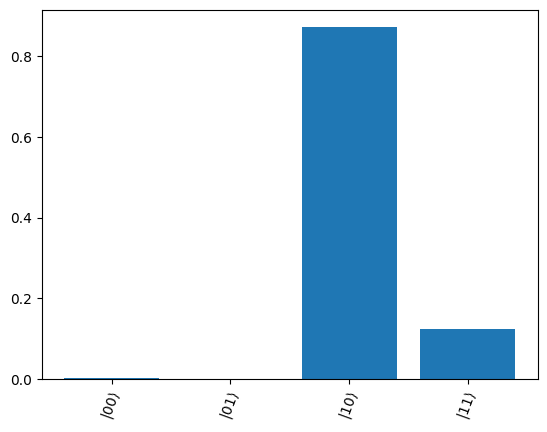

We note that for nlayers=2 and 500 iterations, the objective function does not in this case (although it depends on the initial parameters)converge to the true value of \(-4.5\). However, the we see below that the final wavefunction does have large overlap with the desired state \(|10\rangle\), so measuring the output of the QAOA algorithm will, with high probability, output the correct answer.

[13]:

def print_output(c):

n = c._nqubits

N = 2**n

x_label = r"$\left|{0:0" + str(n) + r"b}\right>$"

labels = [x_label.format(i) for i in range(N)]

plt.bar(range(N), c.probability())

plt.xticks(range(N), labels, rotation=70);

[14]:

c = QAOA_from_Ising(final_params, nlayers, pauli_terms, weights)

print_output(c)

General Case#

For the general QUBO case, we wish to minimize

where \(x\in\{0,1\}^n\) and \(Q\in\mathbb{R}^{n\times n}\) is a real symmetric matrix.

This maps to an Ising Hamiltonian

Below is a simple function which can perform this mapping:

[15]:

def QUBO_to_Ising(Q):

# input is nxn symmetric numpy array corresponding to QUBO matrix Q

n = Q.shape[0]

offset = np.triu(Q, 0).sum() / 2

pauli_terms = []

weights = []

weights = -np.sum(Q, axis=1) / 2

for i in range(n):

term = np.zeros(n)

term[i] = 1

pauli_terms.append(term)

for i in range(n - 1):

for j in range(i + 1, n):

term = np.zeros(n)

term[i] = 1

term[j] = 1

pauli_terms.append(term)

weight = Q[i][j] / 2

weights = np.concatenate((weights, weight), axis=None)

return pauli_terms, weights, offset

Solving portfolio optimization problems with QAOA#

In a simple boolean Markowitz portfolio optimization problem, we wish to solve

subject to

where * \(n\): number of assets under consideration * $q > 0 $: risk-appetite * \(\Sigma \in \mathbb{R}^{n\times n}\): covariance matrix of the assets * \(\mu\in\mathbb{R}^n\): mean return of the assets * \(B\): budget (i.e., total number of assets out of \(n\) that can be selected)

Our first step is to convert this constrained quadratic programming problem into a QUBO. We do this by adding a penalty factor \(t\) and consider the alternative problem:

The variables in the linear terms \(\mu^Tx = \mu_1 x_1 + \mu_2 x_2+\ldots\) can all be squared (since they are boolean variables), i.e. we can consider

which is a QUBO defined by the matrix \(Q\)

i.e., we wish to mimimize

and we ignore the constant term \(t B\). We can now solve this by QAOA as above.

Let us first define a function to convert portfolio data into a QUBO matrix:

[16]:

def QUBO_from_portfolio(cov, mean, q, B, t):

# cov: n x n covariance numpy array

# mean: numpy array of means

n = cov.shape[0]

R = np.diag(mean)

S = np.ones((n, n)) - 2 * B * np.diag(np.ones(n))

Q = q * cov - R + t * S

return Q

We can test this using the qiskit_finance package to generate some stock covariance and mean data:

Note that this was tested with qiskit version 0.39.3 and qiskit-finance version 0.3.4.

[17]:

import datetime

from qiskit_finance.data_providers import RandomDataProvider

[18]:

num_assets = 4

seed = 123

# Generate expected return and covariance matrix from (random) time-series

stocks = [("TICKER%s" % i) for i in range(num_assets)]

data = RandomDataProvider(

tickers=stocks,

start=datetime.datetime(2016, 1, 1),

end=datetime.datetime(2016, 1, 30),

seed=seed,

)

data.run()

mu = data.get_period_return_mean_vector()

sigma = data.get_period_return_covariance_matrix()

Using this mean and covariance data, we can now define our portfolio optimization problem, convert it to a QUBO matrix, and then extract the pauli terms and weights

[19]:

q = 0.5

budget = 3 # Note that in this example, there are 4 assets, but a budget of only 3

penalty = 3

Q = QUBO_from_portfolio(sigma, mu, q, budget, penalty)

portfolio_pauli_terms, portfolio_weights, portfolio_offset = QUBO_to_Ising(Q)

[20]:

# Brute force search over classical results for comparison before we run QAOA

for i in range(2):

for j in range(2):

for k in range(2):

for l in range(2):

x = np.array([i, j, k, l])

print(f"{i}{j}{k}{l}: {np.dot(x,np.dot(Q,x))- portfolio_offset}")

0000: 21.006979417669037

0001: 6.006208358124514

0010: 6.006857249462996

0011: -2.994037697463167

0100: 6.007889613170697

0101: -2.992836964752989

0110: -2.992179512275861

0111: -5.9930299775811875

1000: 5.992965725313347

1001: -3.007905195444355

1010: -3.0070278423618397

1011: -6.008022650501182

1100: -3.0060506769683

1101: -6.006877116105166

1110: -6.005991201884008

1111: -3.006941528402507

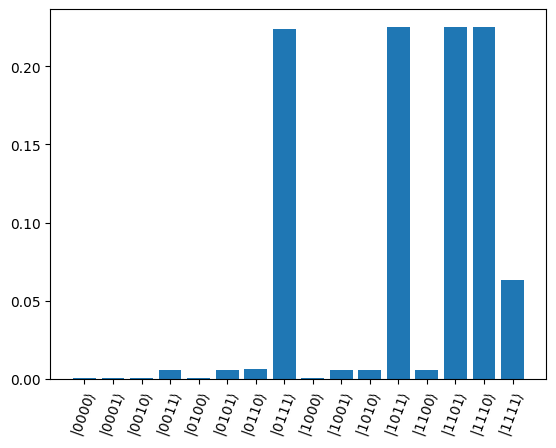

We see that, due to the penalty, the lowest energy solutions correspond to 0111, 1011, 1101, 1110, i.e. the portfolios with only 3 assets.

[21]:

iterations = 1000

nlayers = 3

final_params = QAOA_solve(portfolio_pauli_terms, portfolio_weights, nlayers, iterations)

initial params: [ 0.13778198 -0.75357753 -0.01271329 -0.5461785 -0.1501883 0.36323363]

-4.204754

-5.681799

-5.6837077

-5.6837044

-5.6837053

-5.683704

-5.6837063

-5.683709

-5.6837063

-5.683705

[22]:

c_final = QAOA_from_Ising(

final_params, nlayers, portfolio_pauli_terms, portfolio_weights

)

print_output(c_final)